Grasping Insurance Concepts: Protecting Your Future and Financial Assets

Knowing about insurance is crucial for all people looking to protect their financial future. It acts as a protective barrier against unexpected events which might result in major financial setbacks. A wide range of coverage options exists, each designed for different needs. Yet, numerous people find it difficult figuring out the necessary extent of coverage or understanding the fine print of the agreement. The complexities of insurance may cause hesitation, prompting the need for a clearer understanding on how best to protect one's wealth. What should one consider before making a decision?

Fundamental Insurance Concepts: Key Principles

Insurance functions as a monetary safeguard, guarding individuals and enterprises from unanticipated hazards. Insurance is primarily a covenant connecting the policyholder and the provider, where the customer pays a regular charge to receive monetary protection in case of particular harm or loss. The primary function of coverage is managing exposure, allowing individuals to transfer the burden of potential financial loss to an insurer.

Coverage agreements detail the rules and stipulations, explaining which events are included, which situations are not covered, and how to report a loss. The idea of combining funds is key to insurance; many pay into the system, making it possible to finance payouts to those who incur damages. Grasping the core concepts and language is crucial for choosing wisely. In sum, coverage aims to offer security, guaranteeing that, during emergencies, people and companies are able to bounce back and move forward successfully.

Different Forms of Coverage: A Detailed Summary

Many different kinds of insurance exist to cater to the diverse needs of individuals and businesses. Key examples are medical insurance, that pays for healthcare costs; car coverage, guarding against damage to vehicles; and homeowners insurance, safeguarding property from perils such as theft and fire. Term insurance grants fiscal safety to recipients upon the death of the policyholder, while disability insurance provides income replacement if the person is prevented from earning.

For businesses, liability insurance protects against claims of negligence, and property insurance covers physical assets. PLI, or simply E&O coverage, defends professionals against lawsuits stemming from negligence in their duties. Furthermore, travel insurance provides coverage for surprises that occur during journeys. Each type of insurance is fundamental to handling potential dangers, helping people and companies to mitigate potential financial losses and ensure stability during unpredictable times.

Determining What Insurance You Need: How Much Coverage Is Enough?

Figuring out the right degree of insurance coverage requires a meticulous appraisal of property value and possible dangers. People need to evaluate their financial situation and the assets they wish to protect to calculate the proper insurance total. Sound risk evaluation methods are fundamental to ensuring that one is not lacking enough coverage nor spending too much on superfluous insurance.

Determining Property Value

Determining asset valuation is a necessary phase for understanding how much coverage is necessary for sound insurance safeguarding. The procedure includes determining the worth of personal property, property holdings, and financial assets. Homeowners should consider things such as today's market situation, the cost to rebuild, and asset decline when valuing their home. In addition, individuals must evaluate personal belongings, automobiles, and potential liability exposures associated with their assets. By completing a detailed inventory and assessment, they may discover areas where coverage is missing. Furthermore, this assessment assists people tailor their insurance policies to address particular needs, ensuring adequate protection against unanticipated incidents. In the end, precisely assessing asset worth lays the foundation for smart coverage choices and financial security.

Risk Management Techniques

Gaining a comprehensive grasp of asset worth logically progresses to the following stage: determining necessary insurance. Risk assessment strategies involve recognizing future dangers and figuring out the right degree of insurance necessary to reduce those dangers. This process begins with a full accounting of property, including property, cars, and personal belongings, in addition to an evaluation of future obligations. One should take into account factors such as location, daily habits, and risks relevant to their profession that could influence their insurance needs. Furthermore, reviewing existing policies and identifying gaps in coverage is vital. By quantifying risks and aligning them with the value of assets, it is possible to make sound judgments about the required insurance type and quantity to secure their future reliably.

Grasping Policy Language: Essential Ideas Clarified

Understanding policy terms is essential for traversing the complexities of insurance. Core ideas like coverage categories, premiums, out-of-pocket limits, policy limits, and restrictions are important elements in judging how well a policy works. A firm knowledge of these terms helps individuals make informed decisions when choosing coverage plans.

Types of Coverage Defined

Coverage options offer a variety of coverage types, every one meant to cover specific risks and needs. Standard coverages are liability coverage, which guards against lawsuits; property coverage, securing tangible property; and personal injury coverage, which addresses injuries sustained by others on one’s property. Additionally, broad coverage provides security against a wide range of risks, such as natural disasters and theft. Specific insurance types, such as professional liability for businesses and health insurance for individuals, adjust the security provided. Understanding these types assists clients in selecting appropriate protection based on their individual needs, ensuring adequate protection against possible monetary damages. Each coverage type plays a critical role in a extensive insurance strategy, finally resulting in financial security and peace of mind.

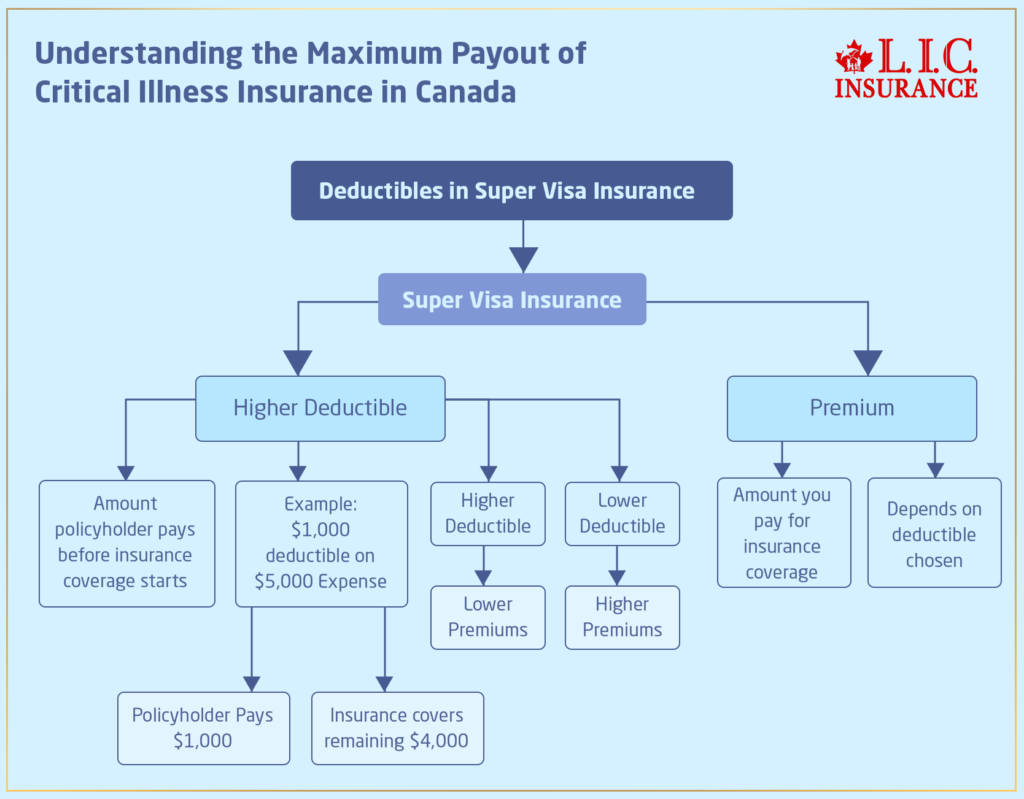

Insurance Costs and Out-of-Pocket Limits

Choosing the appropriate coverage categories is only part of the insurance equation; the monetary elements of deductibles and premiums heavily affect policy selection. The premium is the fee for holding an insurance policy, typically paid monthly or annually. A greater premium often indicates more extensive coverage or smaller deductible amounts. Conversely, deductibles are the figures clients are required to pay themselves before their coverage begins to apply. Opting for a greater deductible can lower premium costs, but it could result in more fiscal liability during claims. Recognizing the trade-off between these two components is crucial for people looking to secure their holdings while controlling their spending wisely. Fundamentally, the interaction of premiums and deductibles defines the total benefit of an insurance policy.

Policy Restrictions

Which factors that can limit the effectiveness of an insurance policy? Restrictions and caveats within a policy define the circumstances under which coverage is denied. Typical exclusions include pre-existing conditions, war-related incidents, and some forms of natural calamity. Caveats might also be relevant to defined benefit levels, requiring policyholders to understand these restrictions completely. These elements can greatly influence payouts, as they specify what financial setbacks will be excluded from payment. Policyholders must read their insurance contracts carefully to find these restrictions, ensuring they are adequately informed about the scope of their protection. Thorough knowledge of these terms is vital for effective asset protection and planning for the future.

The Claims Process: Understanding the Steps When Filing

Making a claim can often be confusing, especially for those unfamiliar with the process. The initial step typically is to alert the insurance company of the incident. This can usually be done through a phone call or web interface. When the claim is submitted, an adjuster may be designated to review the situation. This adjuster will review the details, collect required paperwork, and may even visit the site of the incident.

Following the evaluation, the insurer will verify the authenticity of the claim and the compensation due, based on the policy terms. Claimants should expect to provide access this information supporting evidence, such as photographs or receipts, to facilitate this evaluation. Keeping lines open is key throughout this process; the insured might need to check in with the insurer for updates. In the end, knowing the claims procedure helps policyholders navigate their responsibilities and rights, making sure they get the payment they deserve in a timely manner.

Tips for Choosing the Right Insurance Provider

What is the best way to locate the right insurance provider for their requirements? To begin, they need to determine their specific requirements, considering factors such as the kind of coverage and financial limitations. Meticulous investigation is necessary; online reviews, scores, and customer stories can provide insights into customer satisfaction and the standard of service. Additionally, getting estimates from several insurers enables comparisons of premiums and the fine print.

It is also advisable to evaluate the fiscal soundness and credibility of potential insurers, as this can affect their capacity to fulfill claims. Engaging in conversations with agents can clarify policy terms and conditions, guaranteeing openness. In addition, seeing if any price reductions apply or combined offerings can enhance the overall value. In conclusion, asking reliable friends or relatives for advice may help uncover reliable options. By taking these measures, consumers can select knowledgeably that are consistent with their insurance needs and monetary objectives.

Staying Informed: Keeping Your Coverage Up to Date

After selecting the right insurance provider, individuals must remain proactive about their coverage to ensure it satisfies their shifting necessities. Regularly reviewing policy details is essential, as major life events—such as marriage, acquiring property, or career shifts—can impact coverage requirements. Policyholders must plan annual reviews with their insurance agents to discuss potential adjustments based on these changes in circumstances.

Furthermore, remaining aware of industry trends and shifts in policy rules can offer useful information. This knowledge may reveal new coverage options or price reductions that could improve their coverage.

Watching for competitive pricing may also help find more economical choices without compromising security.

Commonly Asked Questions

In What Ways Do Insurance Costs Change With Age and Location?

Insurance premiums generally go up based on age due to increased risks associated with senior policyholders. In addition, location impacts rates, as cities usually have steeper rates due to increased exposure to accidents and theft compared to non-urban locations.

Am I allowed to alter my insurance company in the middle of the term?

Certainly, policyholders may alter their coverage provider mid-term, but they need to examine the details of their current policy and ensure new protection is secured to avoid gaps in protection or associated charges.

What Happens if I Miss a scheduled premium?

When a policyholder skips a premium payment, their insurance coverage may lapse, which can cause a gap in security. It may be possible to reinstate the policy, but may necessitate paying outstanding premiums and could include fines or increased premiums.

Will existing health problems be covered in medical policies?

Existing medical issues might be included in health plans, but the extent of protection differs per policy. Many insurers impose waiting periods or limitations, though some grant coverage right away, stressing that policy details must be examined completely.

What is the impact of deductibles on the cost of my coverage?

The deductible influences coverage expenses by determining the amount a covered individual has to pay personally before coverage kicks in. A larger deductible generally means reduced monthly payments, whereas smaller deductibles result in increased premiums and potentially reduced personal spending.